December 2019 Monthly Newsletter

December 2019 Monthly Newsletter

Your monthly crypto digest

Welcome to the third issue of the 256 Capital Partners Newsletter.

December is typically characterised by inflection points of trend-reversal in the crypto industry. December 2017 saw the introduction of bitcoin futures at the CME while December 2018 saw the price of Bitcoin fall to around $3,100, returning to a price point seen in early 2017. December 2019 was no different.

We discuss this below and as part of our last newsletter for 2019, we share our outlook for 2020.

Happy Reading!

Fund News

The Multi-Alpha Fund posted our strongest month to date, well over the upper range of our monthly target.

In a similar fractal fashion to 2019 as a whole, December saw a strong downward trend in the first half of the month, bottoming out on the 17th of December at $6,500. Historically, $6,500 represents a point of retracement that was never breached in the bull run earlier on in the year. As a result, our market-neutral funds performed very well due to the market consistently ranging between $6,500-$7,200.

Then in the second half, December was mostly choppy and recovered some losses, ending the month around. Despite the different regime changes, our products managed to adapt to the abrupt volatility conditions and navigated these conditions exceptionally well.

December 2019 Positioning

In a similar fractal fashion to 2019 as a whole, December saw a strong downward trend in the first half of the month, bottoming out on the 17th of December at $6,500. Then in the second half, December was mostly choppy and recovered some losses, ending the month around $7,000.

Seasonal Trend Shifts in December

In an uncanny seasonal observation: Over the past three cycles of three years, mid-December, particularly the 17th of December has been a date that indicates near-exact tops and exact bottoms, signaling a trend reversal from the year or half-year preceding it. This could well be a spurious correlation that may simply indicate human behaviour shifts before the holiday season or start of a new year, but interesting to note regardless.

If the H2 2019 bear market has actually bottomed at $6,500 (and for now it looks like the bottom is holding, with January starting 2020 off strong at a rally up to $8,500), then 17th December 2019 would have marked the bottom date.

Rising Open Interest and Volumes, Low Volatility Remains

Futures open interest, as well as volume, looks to be stabilising and increasing from mid-December lows. When price, open interest and volume move upwards together, this is typically a sign of the beginnings of a bullish reversal.

Spot prices are so far stabilised at a $7000 support so this thesis would see invalidation if we break below again.

In contrast, open interest was climbing up while spot volume was dropping off while the price was falling from July 2019. This meant that it would be likely for prices to continue falling.

December saw extremely low volatility as well as expectations of future volatility, as shown in the chart below. The one month At the Money implied volatility was extremely low, trading between 49-60% in December, meaning that the market expects that large price changes a month ahead was unlikely. The most useful information this gives us is that a majority of the market was becoming used to a choppy, rangey market structure -- a good indicator that that is about to change in January.

Anchored VWAP from volume breakout shows where we’re likely to land or hit

To frame support and resistance bands, we can use a cumulative volume-weighted average price from a point of high volume. In the case below, we use a CME chart to show anchored volume-weighted average point from the highest volume breakout on the 13th of May (highest volume recorded on the CME BTC Futures chart).

It looks like we are headed towards the AVWAP resistance to establish new support; until then, the current support is at the 1stdev lower band area.

2020 Outlook

Below, we dive deeper into a few of our theses for the upcoming year and decade for Bitcoin.

Bitcoin’s correlation with macro risk-off assets should grow, but it will continue to gain its own unique narrative

The path forward for Bitcoin to gain institutional adoption at this stage is to continue trading the way it is. As it already is, Bitcoin provides what no asset class does: a low correlation against other asset classes that institutions are already allocated to (S&P500, bonds, precious metals). And if diversification is the name of the game, there’s no real need for Bitcoin to gain correlation with other asset classes.

For Bitcoin’s narrative as a store of value to grow, it is important for it to have similar behavioural characteristics to gold and assets like crude oil in times of geopolitical crises. But as a bet on some unknown future of money itself, Bitcoin should have some “risky” properties, so it should also reflect riskier equity markets.

We believe this correlation will increase in a world where of infinite QE and potential negative interest rates. Given Bitcoin’s unique 24/7 trading access and nativity to the digital world, unparalleled by physical distance like other assets, its trading profile will definitely continue to be unlike any other asset, which is what makes Bitcoin such an exciting asset to trade.

Looking at a small-time slice of how each respective asset reacted to the news of the de-escalation of the conflict between Iran and the US, we can see that crude oil, gold and BTC futures fell from their gains as the conflict escalated, while S&P500 soared following Trump’s announcement de-escalating the conflict.

It’s important to note that this correlation only lasted for a few days or so, but asset allocators seemed to be pouring capital into Bitcoin as a result of the conflict.

Source: Coinmetrics Real-Time Reference Rates

We continue to monitor these price deviations and correlations real-time. At the moment, it looks like demand from gold is moving towards Bitcoin which is continuing to climb higher.

Short-term Bitcoin volatility should start rising up towards the halving

Volatility is currently priced relatively cheaply from an options point of view, which are currently still trading at around 65% IV at the time of the halving. FTX’s MOVE contracts for Q1 and Q2 imply that BTC will move roughly ~12.5% from its current price now...

Is the market being rational?

Source: @Rptr45 (Twitter)

Bitcoin’s average performance in the year after the 2012 and the 2016 halving shows an average of a +2345% move.

Understandably, it would be difficult for the magnitude of these moves to match the insanity of those days, but we believe that options are underpriced due to the magnitude of the correction in the 2019 mini-bear market.

A simple sentiment check using Google Trends reveals that the search term “Bitcoin halving” has been steadily increasing over the past half a year. Given where it peaked in June, we believe we could see an even more volatile H1 2020 ahead.

New Derivatives such as Options will Explode this Year

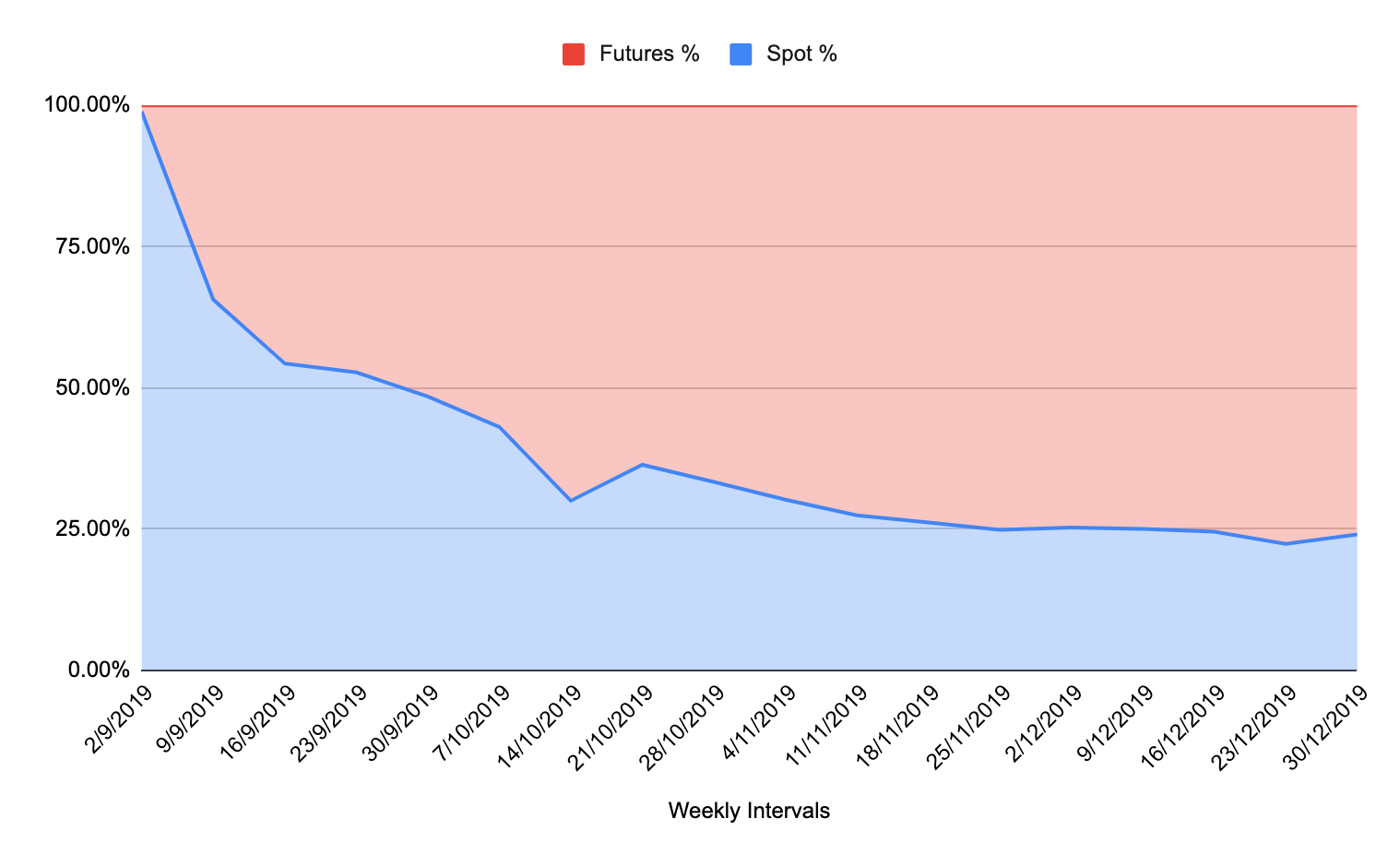

Derivatives saw a fruitful 2019, with many exchanges launching new derivatives platforms -- ByBit, CoinFlex, Binance Futures, FTX and Huobi. For many of these new entrants in the derivatives space, spot volume slowly receded against futures volume. At this stage, futures volume now accounts for over 75% of volume on Binance.

We believe that this trend will only increase with the rise of new derivatives contracts (within crypto) such as options. Options volume has grown exponentially from an average of $2mm to >$50mm traded a day from the beginning of 2019 to today, the launch of institutional CME, Bakkt and OKEx options. Currently, options volumes are only 0.47% of the entire futures market. This year, we believe we will see a second explosion of crypto derivatives, in the style of the perpetual swaps.

Final Words

We’ll be spending January gearing up to launch our two other fund products to our community in February. It’s shaping up to be an operation heavy month before we move to Singapore and Hong Kong to be closer to some of our portfolio funds and fund partners.

As always, please feel free to reach out if you have any comments, feedback or would just like to chat. We’re always delighted to have new partners join us so if this seems like a journey you’d like to be a part of, then please hola our way.

Happy New Year from the 256 Capital Team!

Best,

Cindy & David

The information contained or attached herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations. This presentation may contain forward-looking statements that are within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These forward-looking statements are based on management’s beliefs, as well as assumptions made by, and information currently available to, management. Although management believes that the expectations reflected in these forward-looking statements are reasonable, it can give no assurance that these expectations will prove to be correct. This email is for informational purposes only and does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product, service of 256 Capital Partners as well as any 256 Capital Fund, whether an existing or contemplated fund, for which an offer can be made only by such fund’s Confidential Private Placement Memorandum and in compliance with applicable law. Past performance is not indicative nor a guarantee of future returns. Please consult your own independent advisors. All information is intended only for the named recipient(s) above and is covered by the Electronic Communications Privacy Act 18 U.S.C. Section 2510-2521. This email is confidential and may contain information that is privileged or exempt from disclosure under applicable law. If you have received this message in error please immediately notify the sender.