February 2020 Monthly Newsletter

Disclaimer: This Edition aims to cover events in February and February alone - we will be releasing a special interim-month segment that covers the most recent movements in March shortly.

Welcome to the fifth issue of the 256 Capital Partners Newsletter.

February was characterized by two stories: the first half was euphoria and greed, the second was panic and fear as the global macro environment dragged BTC along with it. In the end, February was a brutal month for Bitcoin, down -9.6%.

In this issue, we analyze how Bitcoin’s position in the macro environment and specifically, how it moves under unprecedented market conditions. In addition, we look at the growing impact of COVID-19 on global markets as well as our thoughts on how upcoming monetary easing policies will affect Bitcoin.

Happy reading!

BTC vs. Gold, Oil & Equities

Bitcoin’s YTD return in February is at +12.27%, which is a seemingly impossible feat for Bitcoin amidst a -15% drawdown in SPY and a -19% drawdown in crude oil. Before we jump into conclusions that Bitcoin is a safe haven in a global macro downturn, the reason Bitcoin is not sensitive to macro downturns is simply because it is not held by the same investors who are sensitive to macro downturns in traditional asset classes.

Institutional investors choose not to panic sell BTC in order to make margin calls (whereas they do gold), because they simply do not own enough BTC.

Even so, fear is infectious across markets and Bitcoin is not immune to it. This was Bitcoin’s first real “test” against a global sell-off, and it seems to have held up well for now, despite its >90% correlation to the SPY over the last few weeks of February.

This could well change — we are betting on our market-neutral portfolio outperforming for the next few months.

Macro Outlook

Bitcoin’s Reaction to Global Markets’ Sell-Off

What’s clear with this chart below is that BTC is still highly correlated with traditional markets during periods of relative “peace” but underperforms gold during macro instability.

What we are seeing here is a clear risk-on vs. risk-off divergence. When markets are risk-on, all asset classes tend to be highly correlated. The moment we move into a risk-off environment, and markets start to de-risk, assets such as gold start to rally above everything else. This is when asset non-correlation becomes important.

As a risk-on asset, we expect BTC to underperform gold in a risk-off environment.

Zooming out, we see that this divergence occurs in August 2015 and sustains for almost a year. BTC depreciated against gold but rallied against USD and SPY. Why did this happen? 2015-2016 marked the end of an oil crisis caused by slowing oil demand from China in the backdrop of massively increased oil production, where oil fell 50% from its $114 peak.

The Impact of COVID-19 on Global Markets

At the time of writing in the first week of March, we’ve seen cases quadruple from 25,000 at the end of January to over 100,000 at the end of February.

The biggest long-term risk to markets right now is the sustained recessionary effects that this pandemic will cause.

The biggest short-term risk, however, is that the world is greatly underpricing the risk of a large scale Wuhan-style COVID-19 pandemic on a global scale.

The chart below confirms this: for instance, only 5 tests per million people have been administered in the US, versus 3,692 per million people in South Korea. This is largely due to CDC regulations in the US preventing cheap and large-scale administrations of the COVID-19 test.

The world has presently approached this exponential problem with linear solutions — the knock-on effects of which could be threatening to the global economy.

Investors would be wise to pursue a defensive portfolio positioning given market uncertainty.

Easing Policies (Currently) have Limited Short-Term Impact on Bitcoin

The question now is, how will the Fed’s easing policies affect Bitcoin?

Since August 2019, the Fed has started announcing aggressive rate cuts from its peak of 2.40% to the current target rate of 1.25-1.50%. At the start of March (at the time of writing), in light of the global equities sell-off last week, the Fed has just announced an emergency rate cut of 50bps, which it has not done since the beginning of the Global Financial Crisis (GFC). The last time the Fed cut three times in a row was also in 2007-2008, from which they have been increasing rates steadily.

Conceptually, it makes sense that stimulation has a positive impact on Bitcoin’s price. However based on how Bitcoin has reacted to rate cuts, there appears to be little evidence that easing policies have any impact on BTC at all as of now.

Examining how Bitcoin has in general reacted to global markets has been a fascinating exercise. It seems clear that Bitcoin is decidedly a risk-on asset at this stage.

Market Positioning

On-Chain Positioning

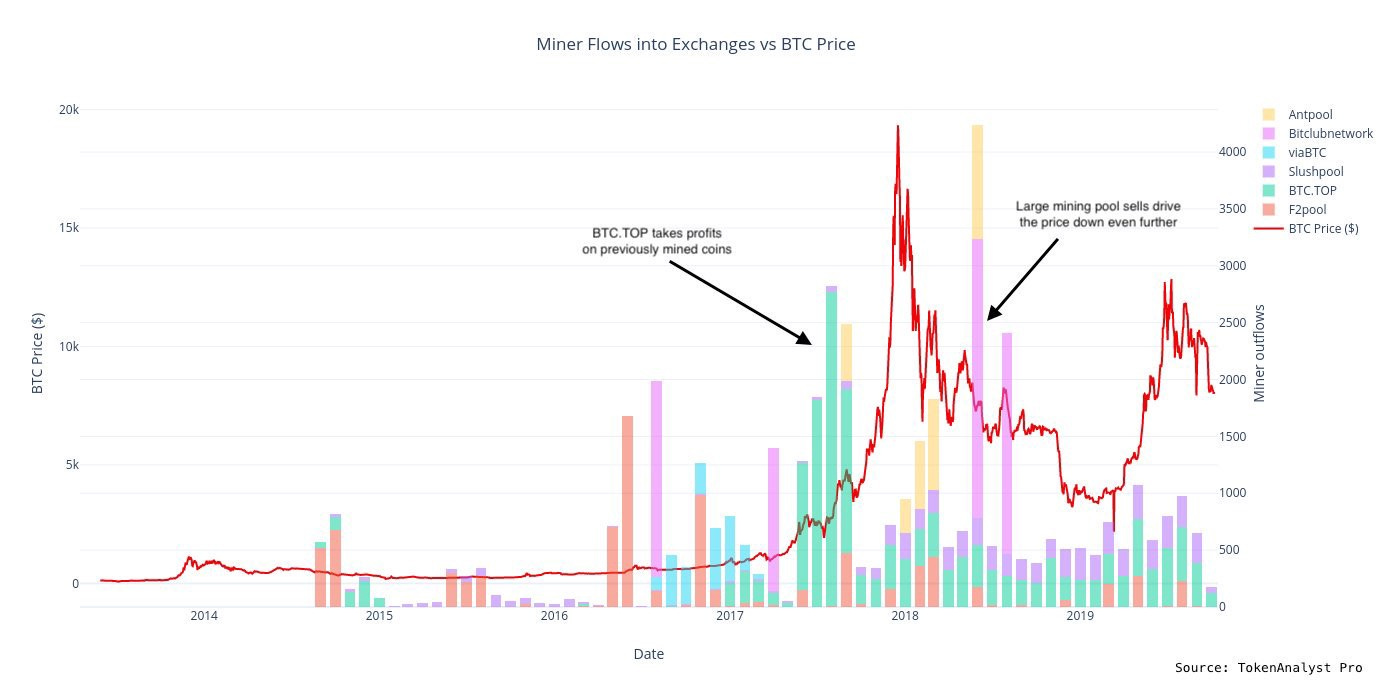

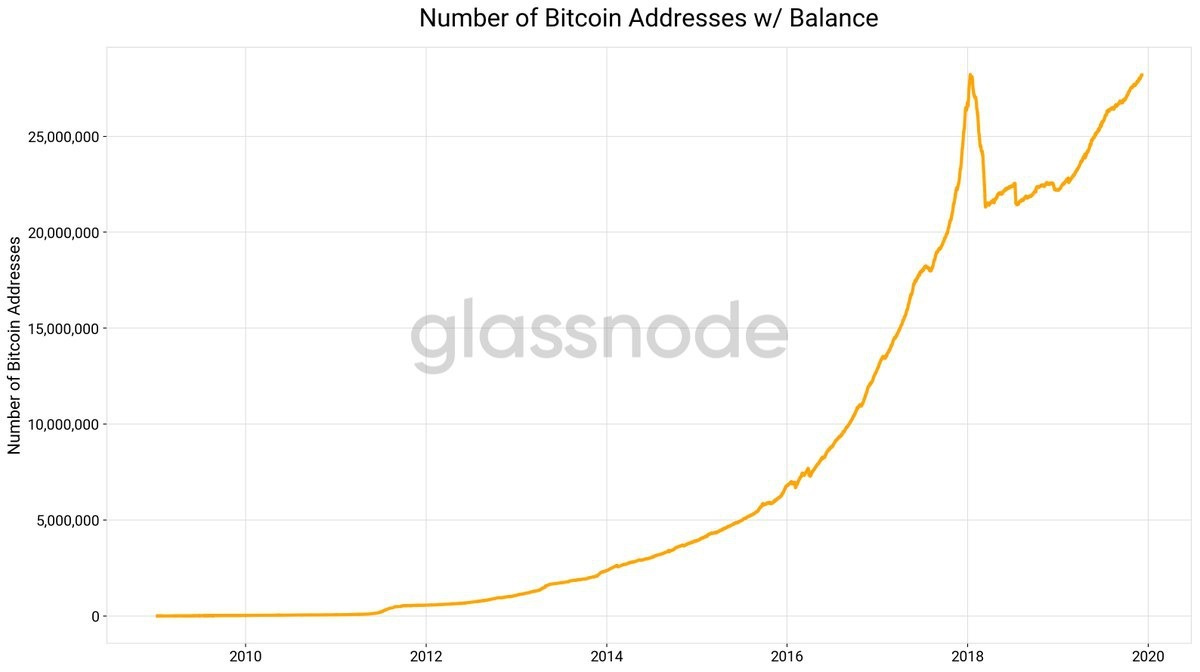

High Address Balances Decreasing

On-chain metrics are also showing declining addresses with >100 BTC. At face value, it seems that many large players are selling off or reshuffling into smaller addresses.

Source: @tokenanalyst

What’s interesting is that while addresses >100 BTC are declining, addresses with <1 BTC are increasing everyday and hitting ATHs. This is clear evidence that larger players are selling off while retails are buying the dip.

SOPR < 1, Most Wallets in Loss

SOPR (Spent Output Profit Ratio) measures from a wallet-to-wallet level the ratio of wallets in profit to the wallets in loss based on the delta of the price at which Bitcoin was acquired per wallet and the current Bitcoin price now. If SOPR < 1, most wallets are in loss since their creation (assuming the price of BTC at wallet creation was their entry price). Currently, SOPR firmly stays below 1. During “bull markets”, this tends to be a good dip entry, but it’s a bearish sign when it does not rise back up and continues further down on a more sustained level (which it looks like now).

Options Positioning

Call-Put Ratio

Options markets are decidedly bearish, with BTC’s call-put ratio for open interest at ~0.5 which means two times puts were traded compared to calls.

Current Market Probabilities based on Implied Volatility

Compare these two charts below. One is the probability of prices being above x$ at maturity in February 2020 and the second is a snapshot taken in March. The options market is more bearish than ever, with the probability of Bitcoin over 10k in June (post-halving) decreasing even further from 38.2% just last month to a meager 22% at the end of February 2020.

Overall, with global macro uncertainty and the escalating COVID19 situation, the market is positioned bearish towards the halving.

Final Words

We spent the first week of March wrapping up our time in Singapore and determining its fit to set up our Asia offices. In short: Singapore represents a great administrative base for the Fund and its stability is very encouraging as a location to grow a team.

The Multi-Alpha Fund delivered another consistent month of performance despite SPY down almost 10% in the same period. The Vega Yield Fund generated some very strong yields across the month due and was net positive, despite the drawdown in Bitcoin towards the end of February. Overall, our funds are very well positioned to weather these downward trending markets so we are very proud to show that our performance is very much uncorrelated to how the market moves. Should you be interested in the specific performance around our products, please reach out to ir@256.capital.

As always, please feel free to reach out if you have any comments, feedback or would just like to chat. We’re always delighted to have new partners join us so if this seems like a journey you’d like to be a part of, then please hola our way.

Hoping you all stay safe during this time of uncertainty.

Best,

Cindy & David

The information contained or attached herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations. This presentation may contain forward-looking statements that are within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These forward-looking statements are based on management’s beliefs, as well as assumptions made by, and information currently available to, management. Although management believes that the expectations reflected in these forward-looking statements are reasonable, it can give no assurance that these expectations will prove to be correct. This email is for informational purposes only and does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product, service of 256 Capital Partners as well as any 256 Capital Fund, whether an existing or contemplated fund, for which an offer can be made only by such fund’s Confidential Private Placement Memorandum and in compliance with applicable law. Past performance is not indicative nor a guarantee of future returns. Please consult your own independent advisors. All information is intended only for the named recipient(s) above and is covered by the Electronic Communications Privacy Act 18 U.S.C. Section 2510-2521. This email is confidential and may contain information that is privileged or exempt from disclosure under applicable law. If you have received this message in error please immediately notify the sender.